IAG Director Sam Botterill unpacks the complexities of risk allocation, including how these are best mitigated and managed between project owners and the market.

IAG Director Sam Botterill unpacks the complexities of risk allocation, including how these are best mitigated and managed between project owners and the market.

The planning and delivery of any infrastructure project requires a thorough consideration of risk, including how these risks are best mitigated and managed between project owners and the market. A project’s risk profile will be of significant consideration in developing a commercial framework that most efficiently allocates and manages risk between clients and their delivery partners. Despite most of us working in infrastructure and dealing with risk allocation every day, it is worth refreshing our knowledge of some of the theories behind risk and its allocation. Including how risk theory might impact our approach to risk allocations on the projects we work on and in our professional lives.

Let’s start with a fundamental question: can risk be transferred? The simple answer, of course, is yes, risk is transferable, but as we will see, the information required to do so is high and often creates barriers. This results in a risk allocation that can run contrary to contemporary risk allocation practices, such as the Abrahamson principles.

In this article, I discuss the potential benefits of identifying any information gaps upfront and incorporating flexibility into the commercial framework to facilitate dynamic planning as the information becomes available.

The Abrahamson Principles

In 1983, Max Abrahamson published his seminal paper Risk Management, where he advocated for effective risk management through the fair and equitable allocation of risk to the party best suited to bear it. As a starting point, Abrahamson proposed a series of principles for the allocation of construction risk. A risk should be borne by a party only where:

- It is within the party’s control (if the risk eventuates, it will be due to the actions of the party);

- The party can transfer the risk through insurance and recover the premium, and this is the most economically beneficial and practical option; or

- The economic benefit of managing the risk lies with the party; or

- To allocate the risk to the party is in the interests of efficiency (including planning, incentive, and innovation) and the long-term health of the construction industry; or

- If the risk eventuates, the loss falls on the party in the first instance, and it is not practicable, or there is no reason under the above principles to cause expense and uncertainty by attempting to transfer the loss to another.

Through these five principles, Abrahamson established a framework by which to determine the party best suited to bear a risk. The construction industry adopted this contemporary framework in what has become known as the Abrahamson Principles.

In the next section, we will discuss the information requirements to achieve the transfer of risk between parties, noting that these requirements are often significantly higher than many realise.

The Risk Environment

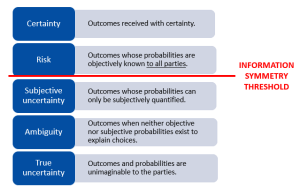

To understand how risk can best be allocated, we must first remind ourselves what is meant by risk and the associated information requirements. In economics, there are five decision-making states:

- Certainty

- Risk;

- Subjective uncertainty;

- Ambiguity; and

- True uncertainty.

A. Certainty

Suppose we imagine ourselves the subject of an experiment whereby if a blindfolded experimenter draws an orange ping pong ball from an opaque receptacle, we stand to win $100. If six orange ping pong balls are placed in the receptacle, then there is a 100% chance of winning the prize, this is a situation of certainty. This is analogous to buying standard, off-the-shelf products, for example. Given the certainty of the product, a decision maker can rely on price and availability, selecting the option that best suits their needs and maximises their benefit.

B. Risk

Now, suppose the experimenter adds four white but otherwise identical ping pong balls to the receptacle; the probability of winning $100 is reduced to 60%. This is a situation of risk, whilst the parties are aware of the probabilities, the outcome cannot be known. Analogously, this would apply when parties to a contract can agree on the probability of encountering certain ground conditions and the consequences of doing so; however, neither party can predict with certainty what ground conditions will actually be experienced. In this situation, the parties could agree on baseline geotechnical conditions with specific contractual mechanisms should circumstances differ from the agreed baseline position.

In situations of certainty and risk, the parties possess all the information, including the objective probabilities of the outcomes; there is information symmetry. The only difference is that with certainty, the outcome is guaranteed; with risk, the outcome is predictable but not assured.

The question, then, is what happens as situations transition from those of information symmetry to asymmetry and the probabilities move from objective to subjective?

C. Subjective Uncertainty

Let us reconsider the second experiment above but replace the four white ping pong balls with four yellow golf balls. Now, assume the experimenter can distinguish between the colours, but we cannot. What is the probability of winning the prize now? Whilst one person might assign equiprobable odds, given their subjectivity, others may assign different probabilities. Given the information available, both approaches are correct; they are, however, specific to the individual or organisation, so it is easy to see why this is a situation of subjective uncertainty.

For example, suppose we return to the geotechnical example above, but this time, the parties predict the conditions to be encountered and allocate the geotechnical risk to the contractor as it is considered within their control under the Abrahamson principles. Even if historical outcomes are used as benchmarks, these conditions can only ever be subjectively known by the parties regardless of how much geotechnical investigation and testing is conducted. This is a situation of subjective uncertainty as the probabilities can never be objectively quantified. The probabilities of any outcome can only be estimated subjectively, meaning that if presented to multiple parties or the same party numerous times, the interpretation may be different or change over time.

D. Ambiguity

Suppose now that the contents of the receptacle contain 100 orange and white ping pong balls of an unknown ratio; how can one determine the odds of winning the $100? The information gap is too large to assign any meaningful probabilities. This is a situation of ambiguity. Take as an example a public infrastructure project that will transcend the lifespan of the initiating government. If there is a change in government during delivery, policy changes may affect the project. Given the lack of available reference information, such changes cannot be objectively quantified ahead of time. People can only fill the gaps using heuristics and biases that are based on their subjective opinions and experiences 1. As the relevant information becomes available, where it differs from the assumptions derived from any heuristics, it will have the inevitable effect of undermining the risk allocation of a project.

E. True Uncertainty

Finally, let’s return to our experiment, but this time, the receptacle is filled with 1,200 ping pong balls of random colours (any colour on the spectrum). What are the odds of the experimenter picking an orange ball and receiving $100? The breadth of colour possibilities and unknown quantities means the information deficit is such that it is impossible to fill and assign any probabilities meaningfully. This is a situation of true uncertainty. Now consider the effects of fat-tailed events such as natural disasters or pandemics on a project. The consequence of an outcome may be worse than any that have preceded it. It is easy to see how true uncertainty can undermine a risk allocation, such as the effects of foreign policy on supply chains.

As a situation descends from certainty to true uncertainty, the information deficit increases to the tipping point where the cost of acquiring the information becomes prohibitive. This deficit raises two challenges: how to maintain information symmetry, and how to fill the information gaps and allocate risk effectively?

Information Symmetry

It is only through a consideration of the information requirements and how information thresholds can be satisfied that one can allocate and transfer risk effectively. In the absence of information symmetry, risk cannot be transferred, only replaced by uncertainty and ambiguity.

Whilst a certain level of information symmetry may be achieved through disclosure requirements, typically, more is needed 2. As the prevalence of arbitration and sealed awards increases, so too does information asymmetry because only the parties to a dispute will know how the information gap was filled. Requiring parties to divulge how any gaps were filled would be both cumbersome and more than likely in breach of any determination, rendering disclosure an ineffective option. Such asymmetry can be exploited during negotiations to the advantage of one party at the expense of the other. This, in turn, will increase the prevalence of zero-sum outcomes and reduce the overall health of the construction industry.

Let us return to the subjective uncertainty experiment, but this time, the experimenter prefers the colour orange to the extent that, given the opportunity, they would always draw orange ping pong balls in preference to yellow golf balls. In this situation, the subject believes they are facing a situation of subjective uncertainty when they are really in a situation of certainty. As the information asymmetry increases, all parties will use their knowledge and information to fill the gaps in a transaction to maximise their bargaining position.

Where risk allocation occurs above the information symmetry threshold, zero-sum outcomes can be eliminated, as the parties possess all the information. This leaves only the quantum (to the extent it is beyond the party’s control) to be agreed upon, which in turn is objectively observable and quantifiable, meaning the parties cannot exploit information. However, where risk allocation occurs below the information symmetry threshold, heuristics and biases are used to fill information shortfalls 3. However, as projects mature and the missing information becomes available, if different from the heuristics used to apportion and transfer the risk initially, this will undermine the allocation and potentially create costly and complex zero-sum disputes whereby the parties exploit the information to their advantage.

Risk Transfer

As discussed above, individuals and organisations will use heuristics based on previous experiences and biases based on their beliefs to fill information gaps; this is where a risk allocation can unravel. Heuristics and biases are subjective and ultimately only placeholders until the actual information becomes available. Should the information differ from what the placeholder expected, it will result in one party gaining a zero-sum benefit at the expense of the other.

So, what can be done? Rather than relying on assumptions and heuristics in an attempt to elevate and transfer uncertainty and ambiguity, contracting parties should consider identifying any information gaps and incorporating flexibility into the commercial framework. By adopting flexibility that is externally verifiable and observable, the parties can eliminate the zero-sum outcomes that could occur when the assumptions used in the initial allocation differ from the information as it becomes available.

In the geotechnical baseline approach discussed above, the parties agree on a risk allocation above the information symmetry threshold based on the available information. However, where an information gap exists, they decide how this will be treated, including, where necessary, pricing. If the encountered ground conditions differ from the baseline conditions, all that needs to be agreed upon is the classification of the conditions and the quantum. Both can be objectively quantified by external third parties if required. By adopting this form of flexibility, future disputes can be reduced in scope to the application of verifiable quanta. This is not open to interpretation, unlike other types of disputes below the information symmetry threshold.

Conclusion

The intention of this article is certainly not to criticise contemporary risk allocation practices but rather to contribute to the risk allocation debate by highlighting that the information required to achieve an efficient allocation of risk may be higher than many realise. The contracting landscape is continually evolving, with new and amended contracting forms such as the NEC 4 making significant headway in providing flexible regimes to deal with risks that sit below the information symmetry threshold. As economic and legal scholars Oliver Williamson and Ian Macneil wrote about at length, transactions occur on a spectrum, which is to say that the risk profile of each transaction is unique 4.

Returning to the discussion above regarding geotechnical conditions, most would agree that the risk profile of a brownfield tunnelling project is such that a total transference of risk would likely attract a significant and unpalatable premium. Rather than complete transference, sharing the risk through agreed baseline geotechnical conditions would reduce risk costing premia and allow the client only to pay additional costs where the conditions differ from the baseline agreed. Conversely, the geotechnical risk profile of a greenfield transmission line may not warrant such an approach as, despite the information requirements for the risk still falling below the information symmetry threshold, the premium for transference is palatable to both the client and market should the risk occur.

Ultimately, where a risk cannot be allocated under the Abrahamson Principles, transacting parties might be better off identifying the information gaps and incorporating appropriate flexibility rather than relying on a party accepting a risk that cannot be accurately estimated at the time of contracting.

In closing, we should consider what role a construction contract plays in the delivery of projects. Whilst there are many opinions on the matter, Ian Macneil suggested that one key role is to anticipate future outcomes and present these terms that are acceptable to the parties at contract award. When viewed through this lens, the reader should consider asking themselves whether they have sufficient information for a contractual risk allocation above the information symmetry threshold or whether there are risks below the threshold. This rule of thumb can then be used as an improved heuristic to ascertain the level of flexibility required in a contract.